ACC506 Accounting Assignment Sample

Here’s the best sample of ACC506 Accounting Assignment, written by the expert.

Executive Summary

The main aim of this report is to prepare the financial statement for Wonderland. In this reference, financial statements are prepared by the analyst on the basis of the available information. This report also compares the company with industry ratio in the context of the liquidity and gross profit margin. In this, it is found that Wonderland is performing well as compared to industry. Along with this, this report also suggests the ways to control the internal mechanisms.

Introduction

In the business environment, it is essential for each company to prepare the record of its financial transaction that happened in the particular time period. In order to prepare the record of the financial transaction, a company prepares the financial statement. The financial statement of accompany includes three major statements such as income statement, balance sheet and cash flow statement. At the same time, in the accounting, in order to evaluate the financial performance ratio analysis technique is also helpful.

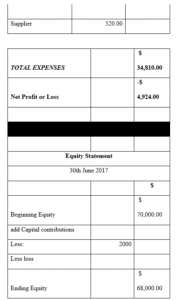

A. Financial Statements

B. Financial Ratio

The above table shows Wonderland is performing well because its current ratio and gross profit margin ratio are high as compare to industry. In this, it is found that current ratio of Wonderland is 7.82 while industry ratio is 1.5-2.7. Its means Wonderland is able to pay its short term liabilities instantly. At the same time, gross profit margin of Wonderland is indentified by 51.61% while industry ratio is 38-43%. On the basis of this, it can be said that Wonderland is also good in the context of gross profit margin.

C. Depreciation Methods

There are various types of method are available under the depreciation which can be use by the wonderland construction supplies in their future investment. The methods are the SLR, declining balance depreciation method, sum of the year digits and units of production deprecation method (Jackson et al., 2010). In order to identify the differences between them then there is need to study below mention methods concepts in which depreciation is charge on the basis of different perspective.

• Straight Line Method (SLR):

It is method in which carrying amount of the fixed assets is reducing over its useful life. This method is developed with the aim to indicate the consumption pattern of the underlying assets and it is one used in case there is no particular pattern in which assets is to be used over time (Rambaud & Richard, 2015). This method is widely used by the companies as it is easy to calculate.

• Declining Balance Depreciation Method:

This method charges high depreciation at higher rate in regards to the previous years of an assets. The value of the assets is reducing as the life of assets progresses. It is calculated in the following manner: – Depreciation per annum= (Net book value-residual value)*Rate%

• Sum of the Years Digits:

It calculates the depreciation through summing the number of years in an assets useful life (Gravelle, 2011).

• Units of production depreciation method:

In This method depreciation is charged based on the expected output or usage of the assets. It is calculated (Cost-Residual Value)/ Useful Life (Bhagoria et al., 2010).

Thus, each method provides major benefit to the company in terms to generate tax saving as depreciated assets are recorded as expenses in the bookkeeping.

D. Inventory Control Method

The methods which are used by the business for maintaining their inventory are the ABC method, EOQ, FIFO and LILO. Likewise, EOQ (economic order quantity) supports to purchase the economic quantity or determine the optimum quantity by considering various factors such as cost of ordering, holding or carrying inventory cost etc (Wee & Widyadana, 2013). It is calculated in the mention manner Q = √2AS/I. FIFO method.

FIFO method includes that sold the first item which is bought at initial level. This means that item is still in stock and such activities help the companies in the period of high price. Whereas LILO indicates that items bought last are need to sold first and such policy does not allow to properly flowing of inventory so because of this, LILO method is least accepted by the companies in order to control the inventory level in their warehouse. ABC method is also playing a crucial role in controlling the expenses of the inventory. However, it assigns cost to each activity that’s help the company to measure the total expenses of the company.

Thus, the above method has a deep impact on the financial position of the business because through estimating the correct inventory level enables the company to reduce their extra investment. Instead of this, it allows the business to make a further investment that’s assist them to improve their financial position in the market.

E. Recommendation

Bank Reconciliation Statement assist in making internal control as it eliminates the maximum mistakes, errors in the bookkeeping which helps in managing the internal operations of the business in an efficient manner. At the same time, bank reconciliation statements also indicate the differences between the entries which assist the business to study the problem areas which is occurring in the business internal process (Fifield et al., 2011). Cash Control should also consider as a suggestion for the companies in order to manage the internal operations. Cash control allows the smoothly flow of operating expenses which result in managing all activities in an appropriate manner. However, if the company manages its daily operating expenses then they become capable enough to control all the activities, stakeholders and able to generate the sufficient revenue. Thus, these both the methods would be well suited to the internal control and they are highly recommended to the business entities for managing their operation.

References

Bhagoria, M., Sadiwala, C. M., & Khare, V. K. (2010) Multilevel inventory techniques for minimizing cost-a case study. Indian Journal of Science and Technology, 3(6), pp. 693-695.

Fifield, S., Finningham, G., Fox, A., Power, D., & Veneziani, M. (2011) A cross-country analysis of IFRS reconciliation statements. Journal of Applied Accounting Research, 12(1), pp. 26-42.

Gravelle, J. G. (2011) Reducing depreciation allowances to finance a lower corporate tax rate. National Tax Journal, 64(4), pp. 1039.

Jackson, S. B., Rodgers, T. C., & Tuttle, B. (2010) The effect of depreciation method choice on asset selling prices. Accounting, Organizations and Society, 35(8), pp. 757-774.

Rambaud, A., & Richard, J. (2015) The “Triple Depreciation Line” instead of the “Triple Bottom Line”: towards a genuine integrated reporting. Critical Perspectives on Accounting, 33, pp. 92-116.

Wee, H. M., & Widyadana, G. A. (2013) A production model for deteriorating items with stochastic preventive maintenance time and rework process with FIFO rule. Omega, 41(6), pp. 941-954.

________________________________________________________________________________

Know more about UniqueSubmission’s other writing services: