AAF042-6 Financial reporting and analysis Assignment Sample

Module code and Title: AAF042-6 Financial reporting and analysis Assignment Sample

1. Introduction

The financial report is a process to disclose financial data as well as taxation of business in the appropriate format as per framework. This report is prepared to analyse the implementation and company of accounting standards in the accounting framework of Barclays PLC. The corporate governance of Barclays PLC has been also analysed in the current report in order to equate differently issues as well as challenges faced to perform business operations.

Apart from this, the strengths and weaknesses of Barclays PLC have been analysed in the current study paper through an analysis annual report as well as by a committee member of the board of directors. The aim of this report is to execute the role of the financial framework as well as regulation to take financial and strategic decisions.

2. Background of company

Barclays PLC is a UK-based universal bank that operates a business in more than 40 countries established on July 20, 1896, in London. The entity has been operating business with nearly 85000 employees as well as revenue of Barclays PLC in 2021 has been existing at 21.94 billion GBP which has increased by 7.95% in the current time compared with last year’s revenue (Barclays, 2022). Barclays PLC has focused on fintech financial technology in order to acquire a better position in the global financial industry as well as enhance satisfaction as well as a feature for consumers.

Key features

Barclays PLC has provided next-generation digital as well as Fintech financial services to different retail as well as other business entities in the UK. Barclays PLC has also sustained the growth of the business by “Delivering sustainable growth in the CIB” as well as identifying different risks and financial crises which is necessary for any business to take appropriate decisions (Barclays, 2022). Barclays PLC has increased its digital platforms as well as delivered Fintech facilities such as auto payments facility to its consumers. 71.8% of clients have been engaged in Barclays PLC through digital platforms.

Objectives

The main objective of Barclays PLC is to provide a double-digit return by “deploying finance responsibly to support people and businesses, acting with empathy and integrity” for a long-term period. Barclays PLC has also focused on a low carbon economy thus, identifying different social investment opportunities for their clients (Barclays, 2022). Barclays PLC has delivered balanced services at a global level by ensuring four different category stakeholders “customers and clients, colleagues, society, and investors”.

3. Discussion accounting standards as a part of complete regulatory framework

Accounting standards refer to a different set of practices as well as a policy which has been considered by different firms as well as entities to record as well as summarise financial transactions. As stated by Vaio and Varriale (2018), Accounting standards have been used to disclose different assets and liabilities with other significant factors of a business which have indicated financial health as well as efficiency of a business. However, the regulatory framework is a legal mechanism that has been used by different business entities to maintain the appropriateness and credibility of financial reports and statements published publicly.

As opined by Wójcik and Sadowska (2018), the regulatory framework has been prepared by different global as well as national financial authorities such as IFRS (international financial reporting framework) has been used in more than 146 countries developed by the financial authority of the UK. Whereas GAAP (General accounting acceptance principle), has been developed by the US and used only US. Accounting is not a total financial regulatory framework due to the difference between accounting standards and regulatory frameworks. There are different reasons for accounting standards not having a complete regulatory framework.

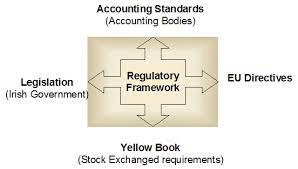

Figure 1: Regulatory framework (Source: Napier and Stadler, 2020)

The financial framework has assisted different stakeholders to observe and measure credibility as well as the authenticity of financial statements and data highlighted in financial statements. Whereas accounting standard has been used by any entity is to present information in a format for publication which can assist different understanding of different financial data to measure financial health.

As stated by Napier and Stadler (2020), the financial framework has been indicating the reliability of financial data which has been considered by different authorities for ascertaining tax liability as well as compliance with different financial rules and regulations.

On the other hand, accounting standard has supported different authorities to evaluate the value of different financial aspects such as total revenue and income for the accelerated tax liability. Nevertheless, the regulatory framework has been ruled to disclose financial data in a proper way with appropriate evidence; however, an accounting standard has been implemented to disclose and record all financial information in a suitable format which has maintained simplicity as well as maintained appropriateness in financial statements. These are key reasons for accounting standards not being a complete past regulatory framework.

Role of accounting standard

Accounting standards have played an important role to maintain simplicity as well as reduce errors in accounting procedures. As opined by Gao (2022), different global, as well as large domestic business entities, need billions of transactions which are complex as well as difficult to record properly in normal bookkeeping. Thus, at that time global business entities need an appropriate framework to record all transactions in a proper format. Accounting standard has assisted global entities to mount simplicity as well as reduced errors and mistakes to record all financial transactions in a proper format.

Figure 2: Regulatory framework (Source: Larkin et al. 2019))

Importance of regulatory framework

The regulatory framework has mainly been developed by different government financial authorities to reduce fraud as well as financial discrimination while operating businesses at the global and domestic level by attracting different stakeholders in Barclays PLC. Thus, the regulatory framework has supported the safe investment of different investors by ensuring better credibility and authenticity based on financial statements and its evidence.

As stated by Larkin et al. (2019), the authenticity, as well as the credibility of financial statements, has been given on appropriateness as well as reliability of evidence which has been representing to the auditor as well as another financial author those are engaged in gives credibility as well as the financial health of business based on financial information in different statements. As stated by Beerbaum et al. (2019), IFRS 2018 has been published by the UK and international financial authorities for maintaining an appropriate regulatory framework in financial statements as well as annual reports of a company.

4. Critical discussion regarding the necessity of corporate reporting in context to the capital markets

The research of La Torre et al. (2020) stated that corporate reporting is referred to as the concept that connects the business to its key stakeholders. This analysis helps to identify that a company can make connections with their stakeholders through corporate reporting. The investor is the primary stakeholder of a company who generally uses corporate reporting as the information included in corporate reporting is helpful in identifying whether the investor can put their capital for investing purposes or not. Therefore, it is stated that corporate reporting is an important element in the capital market for making investments.

In addition, according to the research of Manita et al. (2020), the quality of financial information of the company makes implications on the process of making decisions by the investors. This analysis helps to identify that there is a need for maintaining the quality of financial information for attracting customers.

On the other hand, the research of Lewis and Young (2019) stated that the development of the capital market generally depends on the contribution of an improved financial reporting environment. This research helps to identify that the company is responsible to improve the environment of financial reporting that helps to produce high-quality as well as accurate financial reports on the basis of time that contributes positively to the development of capital markets.

As per the viewpoint of García‐Sánchez et al. (2019), corporate reporting has provided essential information to the participants of the capital market. In addition, this research has also shown that corporate managers acquire both financial and physical resources for the purpose of creating value for the investors of the firm through different business activities.

This analysis helps to identify that corporate reporting plays a significant role in the capital market. On the basis of this analysis, it is represented that Barclays is responsible to provide necessary information on financial or corporate reporting in the capital market as it will be helpful in attracting investors at a high range. In this way, this company will be able to generate increased profit that can lead to increased financial performance as well.

The capital market is a marketplace where different companies have listed themselves to raise funds for business development and growth. Whereas a country has different types of capital markets in order to maintain proper circulation of funds from one person to different businesses and industries.

As opined by Beerbaum et al. (2019), there are some rules and regulations that must be considered by different business entities in order to list themselves in the capital market to acquire funds for business development and increase financial growth. For example, in the UK any company needs to consider IFRS 2018 in order to list themselves in equity or other capital market equity and bonds for acquiring funds.

Figure 3: Regulatory framework (Source: Vaio and Varriale, 2018)

There are different reasons why an organisation needs to implement a corporate reporting framework in order to increase the credibility and authenticity of financial data on which investors are invested in the organisation. As financial corporate reporting consists of some rules and regulations as well as a framework in which business entities are needed to publish or discuss their financial statement which highlights financial health and efficiency.

As stated by Vaio and Varriale (2018), any investor invests in the organisation in the form of equity as well as debenture through analysing financial health and performance in the past year in order to expect a sufficient return from the organisation or executive risk level while investing in the organisation. These are the tourism for organisations that need to implement a corporate reporting framework in their financial reporting system as well as ensure a better film and credibility in the global capital market.

Barclays PLC is also required to consider different rules and regulations of IFRS 2018 regulatory framework in order to enhance their 3 credibilities as well as attract more investors to the organisation. These steps not only support organisations to maintain better corporate responsibility management but also increase the satisfaction and interest of investors to invest in Barclays PLC.

Apart from this, these steps of Barclays PLC have also supported them to reduce errors as well as challenges to publish their financial statements and annual report to the public to attract investors as well as ensure better satisfaction and frame in the global market. Apart from this authority and engaged person in the capital market also executes financial documents and supporting evidence in a proper way and format in order to highlight financial health and performance in the capital market to attract investors and sustain existing investors to promote more investment in Barclays PLC.

As stated by Alam et al. (2019), in the current time, different regulatory authority bodies have focused on increasing the digital reporting framework in order to reduce complexity and increase the credibility of financial statements as well as evidence.

5. Critical analysis and discussion regarding the corporate governance

Corporate governance is considered the system through which businesses are directed as well as controlled as per the viewpoint of Mahmood et al. (2018). This analysis represents the importance of corporate governance in an organisation in order to meet all the responsibilities by the board of directors of the organisation. Good corporate governance has consisted of several benefits for the company such as an improved culture of the company, an increase in accountability, ability to identify issues before their occurrence (Foris et al. 2020).

It is observed from this analysis that the implementation of corporate governance will be effective for the company as it will be helpful in maintaining the image of the brand. In the context of Barclays, this company should also implement good corporate governance to improve its culture, accountability, and identification issues. In this way, this company can improve its overall performance in a significant way.

On the other hand, the research of Kharel et al. (2019) stated that there are five primary issues that a firm can face during the implementation of corporate governance such as conflicts of interest, issues related to oversight, issues in accountability, transparency issues, and ethical violation. Through this analysis, it is stated that a company can implement corporate governance although there is a need to identify issues related to corporate governance and mitigate them.

According to the research of Hakimah et al. (2019), the implementation of good corporate governance standards is helpful in improving the financial performance of a business as well as making a positive impact on the internal efficiency of the company. On the basis of this analysis, it has been represented that Barclays also implements corporate governance as it will be helpful in improving the internal efficiency and financial performance of this business.

In contrast, the research of Zaman et al. (2022) stated that corporate governance is an important factor for a company as it creates a system regarding rules and practices that helps to determine the ways of operating and aligning the interests of all the shareholders of the company. This analysis helps to identify that this company will be able to operate its business effectively and align the interest of all the shareholders which can lead to improved performance.

The research of Behnke et al. (2020) stated that the implementation of a governance framework provides benefits regarding assurance of complying systems with essential security requirements and regulations. On the basis of this analysis, it has been represented that the company can ensure that all the systems are complying with necessary regulations that can lead to improved performance of the company. Therefore, it is stated that Barclays will also be able to improve its performance level by the implementation of good corporate governance.

In addition, the research of Alabdullah et al. (2019) stated that the implementation of good corporate governance makes an impact on the development of capital markets as well as provides influence on the allocation of resources. This research helps to observe that a company can generate the benefit of allocating proper resources and developing capital markets by the implementation of good corporate governance. On the basis of this analysis, it has been represented that Barclays will also be able to allocate its resources and develop the capital market.

In this way, this company can attract more customers as well as investors which can lead to increased generation of profit and return. It can be helpful in increasing the financial position of this company. Through this analysis, it is stated that the implementation of good corporate governance is an important factor that makes a positive impact on business performance in an effective way.

The overall analysis represents that implementation of corporate governance provides numerous benefits to the company that can lead to improved financial performance. Through this analysis, it is stated that the implementation of good corporate governance in an organisation is important to generate increased profitability that can lead to achieving growth in the firm.

6. Identification and analysis of some of the major strengths and weaknesses of current cost accounting

According to the research of Barker and Teixeira (2018), replacement costing is referred to as the method of costing in which the price of an entity would pay for the replacement of an existing asset at the price of the current market with a similar asset. This type of costing included both strengths and weaknesses which are presented below:

Strengths of replacement costing

It is one of the important strategies that help to provide understanding regarding the use of profit and loss (Ahlstrom et al. 2020).

The use of replacement cost accounting is helpful for the company as it calculates the current value and depreciation of the asset and then determines whether replacement is required or not.

Replacement costing is also helpful in assisting cost budgeting by which a company can has become able to develop an effective financial practice for the purpose of preparing finances that provide several benefits.

This method helps to estimate the current value of human resources in a logical as well as representative way (Piwowar-Sulej, 2021).

It is one of the simple methods to determine the cost of a product.

This method represents the efficiency of purchasing products and services.

Weaknesses of replacement costing

This method has included the maintenance of the list regarding the prevailing price of the market as per the viewpoint of Ren et al. (2021). It might not be possible for companies to maintain an updated list on a regular basis. Therefore, it is represented that the maintenance of data is one of the key issues regarding replacement costs.

It generally deviates from the principle of cost due to the issues regarding non-pricing at actual cost.

7. Conclusion

Financial reporting has played an important role in a company for the purpose of providing essential information. The findings of this research show that Barclays is a universal bank that operates its business in several different companies. Accounting standards are a different set of practices and policies that helps to record all financial transactions. Different businesses have used legal mechanism as regulatory frameworks for the purpose of maintaining the creditability of financial reports as well as statements that are published publicly.

In addition, it is identified that corporate reporting plays a significant role in providing information to the capital market by which a wide range of investors can be attracted. In this way, this company has become able to generate profit in a significant way. Corporate governance is an important factor for a company that needs to be implemented as it helps to improve financial performance, ensures compliance system with regulations, and many others. Lastly, it is observed that the replacement costing method has both strengths and weaknesses that have to be considered by this company.

Reference

Journals

Ahlstrom, D., Arregle, J.L., Hitt, M.A., Qian, G., Ma, X. and Faems, D., 2020. Managing technological, sociopolitical, and institutional change in the new normal. Journal of Management Studies, 57(3), pp.411-437.

Alabdullah, T.T.Y., Ahmed, E.R. and Muneerali, M., 2019. Effect of board size and duality on corporate social responsibility: what has improved in corporate governance in Asia?. Journal of Accounting Science, 3(2), pp.121-135.

Alam, M.K., Ab Rahman, S., Mustafa, H., Shah, S.M. and Hossain, M.S., 2019. Shariah governance framework of Islamic banks in Bangladesh: Practices, problems and recommendations. Asian Economic and Financial Review, 9(1), pp.118-132.

Barker, R. and Teixeira, A., 2018. Gaps in the IFRS conceptual framework. Accounting in Europe, 15(2), pp.153-166.

Beerbaum, D., Piechocki, M. and Puaschunder, J.M., 2019. ACCOUNTING REPORTING COMPLEXITY MEASURED BEHAVIORALLY. Internal Auditing & Risk Management, 14(4).

Beerbaum, D., Piechocki, M. and Puaschunder, J.M., 2019. Measuring Accounting Reporting Complexity with customized extensions XBRL–A Behavioral Economics approach. Journal of Applied Research in the Digital Economy (JADE), 1(3).

Behnke, K. and Janssen, M.F.W.H.A., 2020. Boundary conditions for traceability in food supply chains using blockchain technology. International Journal of Information Management, 52, p.101969.

Di Vaio, A. and Varriale, L., 2018. Management innovation for environmental sustainability in seaports: Managerial accounting instruments and training for competitive green ports beyond the regulations. Sustainability, 10(3), p.783.

Di Vaio, A. and Varriale, L., 2018. Management innovation for environmental sustainability in seaports: Managerial accounting instruments and training for competitive green ports beyond the regulations. Sustainability, 10(3), p.783.

Foris, D., Florescu, A., Foris, T. and Barabas, S., 2020. Improving the management of tourist destinations: a new approach to strategic management at the DMO level by integrating lean techniques. Sustainability, 12(23), p.10201.

Gao, J., 2022. Research on Earnings Management under IFRS Framework. International Journal of Science and Research (IJSR), 11, pp.1617-1622.

García‐Sánchez, I.M., Hussain, N., Martínez‐Ferrero, J. and Ruiz‐Barbadillo, E., 2019. Impact of disclosure and assurance quality of corporate sustainability reports on access to finance. Corporate Social Responsibility and Environmental Management, 26(4), pp.832-848.

Hakimah, Y., Pratama, I., Fitri, H., Ganatri, M. and Sulbahrie, R.A., 2019. Impact of Intrinsic Corporate Governance on Financial Performance of Indonesian SMEs. International Journal of Innovation, Creativity and Change Vol, 7(1), pp.32-51.

Kharel, Saramsh. “Transparency and accountability in the Nepalese corporate sector: a critical assessment.” Kharel, S., Magar, S., Chaurasiya, N., Maharjan, S. &Rijal, CP (2019). Transparency and accountability in the Nepalese corporate sector: A critical assessment. Quest Journal of Management and Social Sciences: Corporate Governance Edition 1, no. 1 (2019): 1-25.

La Torre, M., Sabelfeld, S., Blomkvist, M. and Dumay, J., 2020. Rebuilding trust: Sustainability and non-financial reporting and the European Union regulation. Meditari Accountancy Research, 28(5), pp.701-725.

Larkin, P., Leiss, W. and Krewski, D., 2019. Risk assessment and management frameworks for carbon capture and geological storage: a global perspective. Int. J. Risk Assess. Manag, 22(3-4), pp.254-285.

Lewis, C. and Young, S., 2019. Fad or future? Automated analysis of financial text and its implications for corporate reporting. Accounting and Business Research, 49(5), pp.587-615.

Mahmood, Z., Kouser, R., Ali, W., Ahmad, Z. and Salman, T., 2018. Does corporate governance affect sustainability disclosure? A mixed methods study. Sustainability, 10(1), p.207.

Manita, R., Elommal, N., Baudier, P. and Hikkerova, L., 2020. The digital transformation of external audit and its impact on corporate governance. Technological Forecasting and Social Change, 150, p.119751.

Napier, C.J. and Stadler, C., 2020. The real effects of a new accounting standard: the case of IFRS 15 Revenue from Contracts with Customers. Accounting and Business Research, 50(5), pp.474-503.

Piwowar-Sulej, K., 2021. Human resources development as an element of sustainable HRM–with the focus on production engineers. Journal of cleaner production, 278, p.124008.

Ren, Z., Verma, A.S., Li, Y., Teuwen, J.J. and Jiang, Z., 2021. Offshore wind turbine operations and maintenance: A state-of-the-art review. Renewable and Sustainable Energy Reviews, 144, p.110886.

Wójcik-Jurkiewicz, M. and Sadowska, B., 2018. Non-financial reporting standards and evaluation of their use illustrated with example of Polish listed companies. European Journal of Service Management, 27, pp.539-545.

Zaman, R., Jain, T., Samara, G. and Jamali, D., 2022. Corporate governance meets corporate social responsibility: Mapping the interface. Business & Society, 61(3), pp.690-752.