Social Impact Assessment for ICT

Executive Summary

The aim of this report is to analyze the disruptive innovation and its impact on the workforce’s employment. However, the increasing trend of mobile technology gives rise to the innovation of varies application and digital payment is the one which gain high acceptances in current business scenario.

So, the payment through facial posture is the new disruptive technology which changes the payment process and support the secured transaction. This technology supports the individuals in term to not carry the handset always on any store or assist the business to reduce customer complaints about the improper payment facilities.

Moreover, this technology implementation also demands for the necessary ICT skills among the individuals so that the best experiences can give to the customers. However, this technology also affect the workforces of countries as with the increasing innovation in IT sector, the requirement for workers get reduced and this result in influencing their livelihood as without job, it becomes difficult to improve their standard of living.

This problem is increasing in rapid manner in current business environment where people struggle for their livelihood.

Appendix A.. 11

- Identify what ethical responsibilities the existing ICT workforce has to support the integration of these technologies into businesses and daily life. 12

- What recommendations could you make to minimize the disruption these technologies. 13

This report is based on evaluating the mobile payment application which has been developed to make payment for a product or a service through the help of portable electronic devices which includes smartphones and electronic devices(Jin, et al., 2017). As the report progress it will also discuss about the description of mobile payment along with identifying how the technology could disrupt the current way society functions.

Moreover, during this report, it will also discuss the risk and opportunities that are associated with mobile payment options. The appendix b of this report will discuss ethical responsibilities that are associated with the ICT workforce. Finally, recommendations will also be provided to minimize the disruption of the technologies.

The increasing technology put pressure on the firm to get incorporated it into the business process. The technology adaptation also demands for the skilled technical staff which can manage the technology. So, the installation of advanced technology is important to sustain for longer duration in this competitive business environment(Sessums, et al., 2016).

However, the mobile technology recently includes the disruptive innovation which gives rise to strong transformation to many business sectors. This is the mobile payment through application of pay by face and it is an secured innovative technology in which customers can make purchase simply posing behind the point-of-sale machines equipped with cameras.

These are linking an image of their face to a digital payment system or bank account. For this payment pattern, the customer or individual does not require to bring the mobile phone. So, this disruptive innovation proves to be quite beneficial in term to solve the major problem of stolen of mobile set and access individual information from the card payments.

This facial recognition technology tend to achieve greater acceptances by the individuals or different companies as it reduces the burden to carry out the handset all time and for firms, it become easy for them to get an delay in customer services and enhance their experiences through gain high level of satisfaction(Ebersold & Glass, 2015).

This technology can be adopted by the telecommunication firms, IT firms and retail sectors. These business entities majorly get a profit with the incorporation of this technology.

In order to incorporate the application face by pay, it is important for business to have the workforces which possess ICT or necessary technical skills as these expertise people able to manage different processes for installation of application into the business(Theguardian, 2019).

This technology proves to be disruptive for the human resources as after installation of this system in store or mobile then the requirement of large workforces get reduced which could create the problem of unemployment. But at the same time, this application supports the security in mobile payment and reduces the chances of unauthorized access of confidential information.

Therefore, it can be stated that facial payment application in mobile phones tends to be disruptive technology which change the digital payment system.

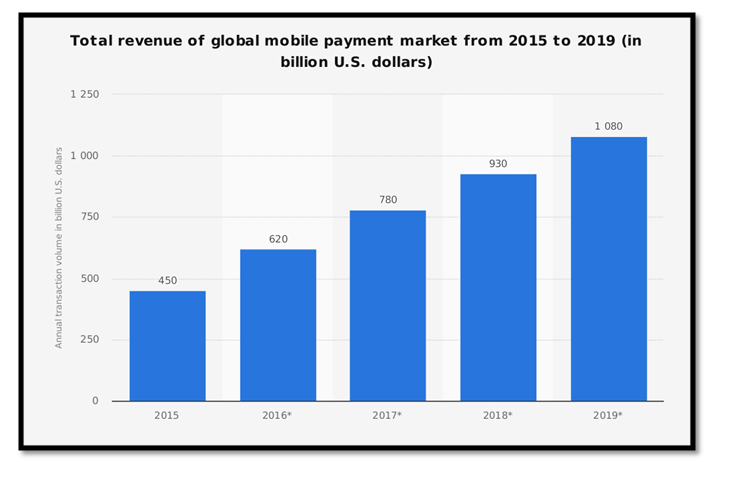

Figure 1: Total revenue of global mobile payment market from 2015 to 2019 (in billion U.S dollars)

Source: (Statista, 2019)

2 a. Description of the technology

The mobile payment system is generally referred to as the payment services that are operated under financial regulation which are performed from or via a mobile devices. Mobile payment options are also used to send money to friends and family members such as with the application of PayPal and Venmo.

The application of mobile payment has transformed the shopping experiences for the customers such as mobile payment options are made available on-site at stores by scanning the barcode on an app through the phone(Dahlberg, et al., 2015).

The mobile payment options have made it easier for the customers to shop conveniently which provides them enriched experiences. Mobile payment options come with upgraded technologies that benefit in increasing efficiency along with providing seamless transactional activities.

Mobile payment options come with a fingerprint scan or PIN input that makes the mobile payment options more secured and reliable(Cardina & Huggins, 2015).

Each of the transactions made with the help of a mobile payment system generates security codes that encrypt all the transactional information and is much more secure than using a physical card.

The mobile payment system is secured with the help of digital authentication which allows the users to use their smartphone devices as their ATM card and scan them to make payments. Using smartphones for payment increases safety features because it is controlled by the authentication of the user and smartphone brand which increases its reliability among the customers.

Artificial intelligence is also used for mobile payment system which uses m-POS units which are wireless devices that replicate traditional cash registers and sale terminals(Dorso & Alao, 2015).

The mobile payment system is also secured with the help of two-factor authentication, this technology helps the users to secure their personal information so that the risk of data theft can be minimized. The mobile payment system also comes with automated payments, intuitive click & Brick that provides opportunities to the customers to increase their shopping experiences.

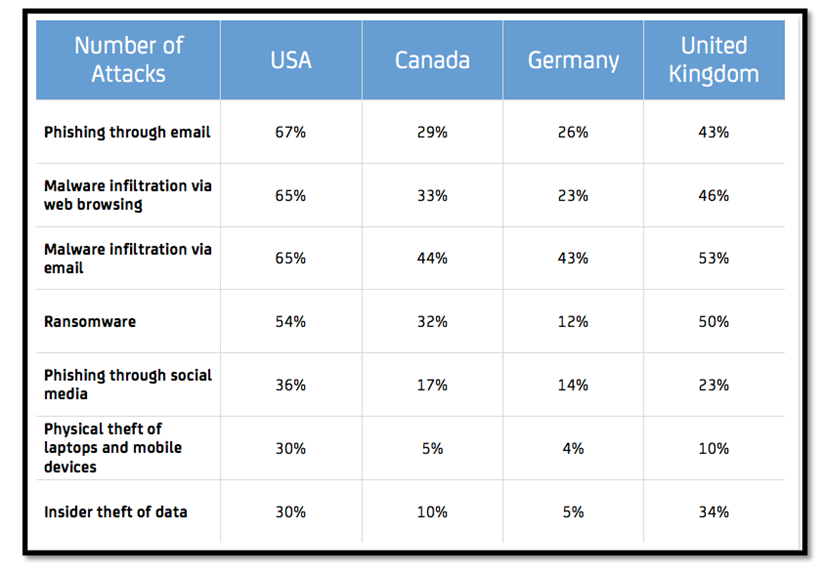

Figure 2: Increase in number of attack due to mobile payment system

Source: (Archiware, 2019)

2 b. How technology could disrupt the current way society functions

The development of the mobile payment system can disrupt the current way of social functions such as not everybody has the knowledge of using digital transactions and hence its reach is only limited to urban and semi-urban centers and therefore it becomes challenging in implementing mobile payment systems in rural areas and among illiterate people.

Advancement in the mobile payment system also impacts other business organisation such as its impacts on street shopping vendors and small SMEs business. It has been noticed that most of the street shop vendors and SMEs operate in cash as a result of which it might affect their business operations(Economictimes, 2019).

Cash transactions are used to purchase inventories and other resources in rural areas due to the non-availability of internet connections. Hence, if the mobile payment system fully takes over then it becomes difficult for the small SME business ventures to operate their business and achieve success.

Moreover, it has also been noticed that due to the implementation of a mobile payment system it also impacts the job such as in developing countries where most of the small traders and farmers rely on cash transactions they might have to lose the job due to the mobile payment system.

Furthermore, it has been noticed that due to the application of the mobile payment system it also impacts the lifestyle of the people such as due to lack of proper knowledge among the people it increases the risk of data theft(Oliveira, et al., 2016).

It has been noticed that people lacking proper knowledge of operating cash related transactions through mobile applications expose their data as a result of which it increases cyber-attack and risk of data theft. Another challenge that has been noticed with the mobile payment system is that any form of digital payment such as internet banking and credit cards involves transactional fees which are not the case with cash transactions.

Therefore, evaluating the fact it has been noticed that the mobile payment system might disrupt the current way of society functions.

This report was based upon a mobile payment system where evaluating the technology it has been identified that it benefits the people in saving time along with increasing their experiences. Discussions have been made concerning the impact of mobile payment systems on other organisation as well as among other professional jobs.

As the report progress, it has also discussed risk and opportunities associated with a mobile payment system such as lack of knowledge increases risk and ease of payment and data security provides opportunities. Finally, ethical responsibilities that exist with the ICT workforce to support the integration of technologies have also been mentioned in this report briefly.

Archiware, 2019. Cyber-attacks-backup-medium-maximum-security. [Online]

Available at: https://blog.archiware.com/blog/cyber-attacks-backup-medium-maximum-security/statistik-malware-spotlight-6-2017-ohne-rahmen/

[Accessed 13 October 2019].

Cardina, D. & Huggins, L., 2015. U.S. Patent. Systems and methods for randomized mobile payment, 9(117), p. 210.

Dahlberg, T., Guo, J. & Ondrus, J., 2015. Electronic Commerce Research and Applications, 14(5), pp.. A critical review of mobile payment research, 14(5), pp. 265-284.

Dorso, G. & Alao, R., 2015. U.S. Patent. Systems and methods for fast mobile payment, 9(213), p. 972.

Ebersold, K. & Glass, R., 2015. Issues in Information Systems. THE IMPACT OF DISRUPTIVE TECHNOLOGY: THE INTERNET OF THINGS, 16(4), p. 10.

Economictimes, 2019. Going-cashless-is-it-good-for-you. [Online]

Available at: https://economictimes.indiatimes.com/wealth/spend/going-cashless-is-it-good-for-you/articleshow/55908649.cms?from=mdr

[Accessed 12 October 2019].

Jin, Y. et al., 2017. In International Conference on Mechatronics and Intelligent Robotics . In: Study on security of mobile payment. London: Springer, Cham, pp. 123-127.

Oliveira, T., Thomas, M., Baptista, G. & Campos, F., 2016. Computers in Human Behavior. Mobile payment: Understanding the determinants of customer adoption and intention to recommend the technology, 61(1), pp. 404-414.

Selvadurai, J., 2013. Legal And Ethical Responsibilities In Mobile Payment Privacy, 5(1), p. 10.

Sessums, L., McHugh, S. & Rajkumar, R., 2016. Jama. Medicare’s vision for advanced primary care: new directions for care delivery and payment, 315(24), pp. 2665-2666.

Slade, E., Williams, M., Dwivedi, Y. & Piercy, N., 2015. Exploring consumer adoption of proximity mobile payments. Journal of Strategic Marketing, 23(3), pp. 209-223.

Statista, 2019. Mobile-payment-transaction-volume-forecast. [Online]

Available at: https://www.statista.com/statistics/226530/mobile-payment-transaction-volume-forecast/

[Accessed 13 October 2019].

Taylor, E., 2016. Mobile payment technologies in retail: a review of potential benefits and risks. International Journal of Retail & Distribution Management, 44(2), pp. 159-177.

Theguardian, 2019. Smile-to-pay-chinese-shoppers-turn-to-facial-payment-technology. [Online]

Available at: https://www.theguardian.com/world/2019/sep/04/smile-to-pay-chinese-shoppers-turn-to-facial-payment-technology

[Accessed 13 October 2019].

c. Identify what risks and opportunities the technology provides

The risk that has been identified with the mobile payment system is that due to lack of proper transactional process, the personal information of the customers is exposed and gets vulnerable to data theft and risk of cyber-attack.

The risk of cyber-attack leads to data loss and personal information of the customers which devalues customers’ trust towards mobile payment options. In developing and under-developing countries lack of proper training and information is a huge risk that might disrupt the overall functions of the mobile payment system(Taylor, 2016).

Finally, the lack of proper infrastructures such as the availability of internet and capital investment could also restrict the growth of the mobile payment system. Contradictory to it the opportunities that have been identified for the mobile payment system include saving the time of the people, digital form of payment system enables the customers to make a purchase and pay through a digital platform that is easier and convenient(Slade, et al., 2015).

Furthermore, it has also been noticed that it also helps in developing the economy such as using a mobile payment system it helps in circulating liquid money that boosts the economy and helps in reducing illegal activities. Compared to cash transactions digital form of payment are easier to carry and safe to handle as all the information are stored in smartphones and secured by two-factor authentication.

d. Identify what ethical responsibilities the existing ICT workforce has to support the integration of these technologies into businesses and daily life

Ethical responsibilities that the existing ICT workforce needs to support the integration of mobile payment system into business and daily life includes the protection of nonpublic personal information. These ethical responsibilities are maintained under section 501 of GLBA, where all the business organisation is obliged to protect the security and confidentiality of the customers.

The information that is provided by the people to the business organisation is being stored and secured so that under no circumstances the information gets leaked or is used by third-party vendors for illegal activities(Selvadurai, 2013). Under section 501 of GLBA the organisation also uses the technology to provide safety of the consumer privacy data by establishing appropriate administrative and physical safeguards.

Furthermore, under the Gramm-Leach-Bliley Act (GLBA) it becomes essential for the organisation to encrypt mobile P2P payments which are secured with the help of emails and phone numbers. Therefore, the ethical responsibility that is used by the ICT workforce manages them to protect unauthorized access and anticipated threats.

e. What recommendations could you make to minimize the disruption these technologies

The recommendations that are being provided to the organisation would help them in improving the mobile payment system along with upgrading the technologies upon which it becomes easier to minimize the threat of disruption of technologies.

The first recommendation is about securing data storage in regards to privacy information. It is encouraged by the organisation not to store any nonpublic information on mobile devices. Rather it is recommended that mobile devices needs to be used for the purpose of reading payment information but not to store public information.

NFC chip could be used to store payment information because NFC based payment methods act similar to the contactless payment card system, which can be used to maintain security and confidentiality. Therefore storing payment information in the NFC chip is justified.

The next recommendation for the business organisation in regards to the mobile payment system includes using integrity and ethical sense in designing and implementing mobile payment applications. The information that is accessed by the organisation needs to be secured so that all the information of the customers can be stored and ethical responsibilities can be maintained within the organisation.